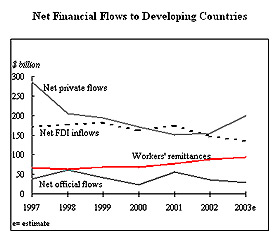

Net private capital flows to developing countries as a whole rebounded to US$200 billion in 2003, up from US$155 billion in 2002, but most of the increase is concentrated in just a few relatively better-off countries, while official development assistance to poor nations increased only marginally, says the annual World Bank report, Global Development Finance 2004.

"The rebound in capital flows to some of the larger countries is encouraging, and reflects an improving global economic picture," said Francois Bourguignon, the World Bank's Chief Economist. "But we are concerned about official aid flows, which are of critical importance to the poorest countries. They have increased only slightly, and last year remained well below the levels required to achieve the Millennium Development Goals (MDGs),"

The increase in net private flows -- bonds and bank loans -- most of which went to Brazil, China, Indonesia, Mexico and Russia, is the major factor in an overall increase in net capital flows to developing countries from all sources, public and private, to US$228 billion in 2003 from US$190 billion in 2002. Net private capital flows rose to all developing regions, except the Middle East and North Africa. These increases are due partly to low interest rates in the industrial countries, and reflect a strengthening global economic recovery. They have also been prompted by sounder fiscal policies in many developing countries, as well as structural reforms.

Despite the overall increase in capital flows to developing countries, however, net resource transfers from rich to poor countries remain negative. Also, net official development assistance (ODA) rose by only US$6 billion to US$58 billion in 2002, with half of this increase is accounted for in debt relief and some administrative costs to donor agencies, rather than new resources to developing nations. Another US$1 billion of the increase consists of new flows to Afghanistan and Pakistan.

"This small increase in ODA is troubling, especially given the failure to reach agreement at last year's WTO meeting in Cancún on reducing agricultural subsidies and trade barriers," Bourguignon said. "We hope to see progress in the next year with Northern countries delivering on their promises at recent international conferences in Monterrey, Doha, and Johannesburg to make development a top priority."

As a whole, the developing countries ran current account surpluses totaling US$76 billion, or about 1.1 percent of GDP. These surpluses-concentrated in Russia, China and Saudi Arabia-now coincide with a large buildup of a few developing countries' reserves totaling more than US$1.2 trillion. China, India and a few others account for a large proportion of these reserves and have invested large volumes in the financial markets of developed countries.

"This shows deepened interdependence in the world economy, with global capital flows, trade and exchange-rate policies more intricately linked than ever before," said Mansoor Dailami, lead author of the report. "The challenge is to increase the flows to developing countries in a way that is sustainable, which requires channeling them to countries with good policies and into investments that spur long-term growth and poverty reduction." With this in mind, the GDF outlines mechanisms to re-ignite slumping investment in infrastructure, as well as trade finance in developing countries.

The increase in capital flows reflects improved global economic growth, which rose from 1.8 percent in 2002 to 2.6 percent in 2003, and which is forecast to jump to 3.7 percent this year. Developing countries, as a group, grew by an estimated 4.8 percent in 2003, and are expected to register 5.4 percent growth in 2004, which would surpass their previous 5.2-percent record high in 2000.

This new buoyancy is prompted by the easing of fiscal and monetary policies in the rich countries, especially the United States, and by a 10-percent rise in non-oil commodity prices, upon which many developing countries heavily depend for foreign exchange. Also, as many developing countries accumulated surpluses and moved to rely on equity finance, they have improved their external liability positions. Total external debt of the developing countries was 37 percent of GDP in 2003, down from 44 percent in 1999.

These trends have been mutually reinforcing, as they coincide with sounder fiscal and monetary policies in many developing countries, as well as the adoption of flexible exchange-rate systems which, together, tend to reduce the incentives to borrow in foreign currency. The average sovereign credit rating for developing countries reached its highest level since 1998, with several countries, including India, Russia and Turkey, receiving upgrades from the major credit rating agencies in 2003. Also, the average spread on emerging-market bonds (EMBI+) fell from more than 765 basis points at the end of 2002 to just 385 basis points in early January 2004, before rebounding to 430 basis points in late January.

There is a risk, however, that fiscal deficits in high-income countries, which have widened every year since 2000, could imperil the flow of capital to the developing countries.

"Fiscal deficits in the developed countries have widened to 3.7 percent of GDP," said Uri Dadush, Director of the World Bank's Development Prospects Group. "If uncorrected, fiscal imbalances could push real interest rates higher globally as the recovery builds, potentially dampening capital flows to low and middle-income countries, as the public sector in the high-income countries competes with developing countries for access to global savings."

While overall private flows to developing countries increased in 2003, foreign direct investment declined for the second consecutive year, dropping to US$135 billion, down 24 percent from its 2001 peak of US$175 billion. Much of this decline can be attributed to weaker FDI in the services sectors such as telecommunications and energy, in which the privatization cycle of the late 1990s has now wound down, and where a few countries that were large recipients of services-bound FDI, such as Argentina, suffered a crisis.

A significant and growing new source of capital for developing countries is remittances sent home by migrants working in rich countries, which have climbed steadily since 1998, reaching US$93 billion in 2003, up 20 percent from 2001. They are now the second most important financial flow to developing countries after FDI, and represent almost double the flows of official aid.

The small increase in official aid flows is accompanied by a drop in net non-concessional lending by bilateral aid agencies, from -US$8.8 billion in 2002 to -11.8 billion in 2003. Multilateral institutions' net non-concessional lending also dropped in 2003, from US$7.2 billion to US$0.1 billion, largely due to the absence of major crises requiring emergency packages, and prepayment of loans to the World Bank, notably by China, India and Thailand.

Capital flows open opportunity

The increase in private capital inflows offers significant opportunities for developing countries to invest in infrastructure and facilitate trade finance to foster a self-reinforcing cycle of sustained capital flows, economic growth and poverty reduction.

Since 1997, every important measure of infrastructure finance to developing countries, including total external finance, project finance, and investment with private participation, has declined by at least 50 percent. This downturn, led by the East Asia, Russia and Brazil crises of the late 1990s, has been accentuated by retrenchment by major commercial banks, and a weakening of the global infrastructure industry.

But infrastructure needs in developing countries are both pressing and largely unmet. About 1.1 billion people do not have access to safe drinking water, 2.4 billion do not have adequate sanitation, and 1.4 billion have no power. The cost of needed infrastructure investments in developing countries is estimated at US$120 billion a year from now to 2010 in the electricity sector, and US$49 billion a year up to 2015 for water and sanitation.

The World Bank report recommends that developing countries seek to tap international capital to meet this demand for infrastructure financing by, among others, establishing transparent rules with the assurance that contracts will be respected, strengthening local capital markets, developing public-private risk mitigation instruments, and helping public providers of infrastructure services achieve commercial standards of creditworthiness. It also calls on multilateral agencies to support countries in pursuing these reforms.

As trade accounts for about one-half of the gross national income of developing countries, financing that trade is important to a country's development prospects, the Bank report says. Trade finance, provided by commercial banks, export credit agencies, multilateral development banks, suppliers and purchasers, has fluctuated since the early 1980s, but on average its growth has been about 11 percent a year. In 2003, trade finance commitments by international banks totaled US$23.7 billion. Global Development Finance calls on countries and multilateral agencies to take steps to increase trade finance, especially for poor countries. With creditors' risk mitigated by securing finance with the traded goods, such countries can open their way to broader access to financial markets.

While the global economy is clearly on a track to recovery, the pace of the upturn and likely prospects is varied across developing regions. Some highlights:

· East Asia led the world with 7.7 percent growth, largely driven by China, as it represents two-thirds of the region's GDP, but also because it is becoming an important export market for other countries in the region.

· Led by a tripling in capital spending growth, GDP in Eastern Europe and Central Asia was 5.5 percent in 2003, up from 4.6 percent in 2002.

· Buoyant growth propelled by domestic consumer demand and relief from drought in India helped South Asia reach 6.5 percent growth. Workers' remittances and growing FDI are also increasingly important factors in South Asia's growth and prospects.

· Despite the Iraq war, GDP in the Middle East and North Africa rose by 5.1 percent, up from 3.3 percent in 2002, with oil exporters leading the way on the strength of higher oil prices.

· Despite a booming oil sector in West Africa, Sub-Saharan Africa's overall growth slowed to 2.4 percent , down from 3.3 percent in 2002, as adverse weather conditions dampened agricultural production, while civil conflict remained a factor in several countries.

· Latin America is experiencing a slow recovery, with regional GDP up 1.3 percent in 2003. Excluding the countries emerging from crises, the strongest performers were Chile, Colombia and Peru. With recovery broadening to Mexico and Brazil, growth is projected to reach 3.8 percent this year.

Global Real GDP Growth

|

2002 |

2003e |

2004f |

2005f |

2006f |

World |

1.8 |

2.6 |

3.7 |

3.1 |

3.0 |

|

High income countries |

1.4 |

2.1 |

3.3 |

2.6 |

2.5 |

|

Developing countries |

3.4 |

4.8 |

5.4 |

5.2 |

5.0 |

|

East Asia and Pacific |

6.7 |

7.7 |

7.4 |

6.7 |

6.3 |

|

Europe and Central Asia |

4.6 |

5.5 |

4.9 |

4.8 |

4.7 |

|

Latin America and Caribbean |

-0.6 |

1.3 |

3.8 |

3.7 |

3.5 |

|

Middle East and N. Africa |

3.3 |

5.1 |

3.7 |

3.9 |

4.0 |

|

South Asia |

4.3 |

6.5 |

7.2 |

6.7 |

6.5 |

|

Sub-Saharan Africa |

3.3 |

2.4 |

3.4 |

4.2 |

3.9 |

Financial Flows to Developing Countries

|

|

1997 |

1998 |

1999 |

2000 |

2001 |

2002 |

2003e |

|

FDI |

171 |

176 |

182 |

162 |

175 |

147 |

135 |

|

Net private flows |

286 |

206 |

194 |

171 |

151 |

155 |

200 |

|

Net official flows |

38 |

61 |

42 |

23 |

55 |

35 |

28 |

|

Workers' remittances |

66 |

63 |

68 |

68 |

77 |

88 |

93 |

Note: e=estimate, f=forecast

(China.org.cn April 20, 2004)